Having an insurance claim rejected can be one of the most frustrating experiences for any policyholder in India. Whether it is a health insurance claim after a costly hospitalisation, a life insurance death benefit claim by a grieving family, a motor insurance claim following an accident, or a property insurance claim after natural disaster damage — a wrongful rejection can leave you financially devastated at the worst possible time. The good news is that Indian law provides robust protections, and you have every right to fight back.

This comprehensive guide explains the common reasons insurers reject claims, your legal rights as a policyholder, the step-by-step process for sending a legal notice for insurance claim rejection, the grievance redressal mechanisms available to you — from the IRDAI to the Insurance Ombudsman and Consumer Forum — and how to build the strongest possible case to get your rightful claim settled.

Understanding Insurance Claim Rejection

An insurance claim rejection occurs when an insurance company refuses to pay the benefit or indemnity that a policyholder (or their nominee/beneficiary) has claimed under the terms of a policy. The insurer typically issues a written repudiation letter citing specific grounds for the denial. Claim rejection is distinct from claim short-settlement, where the insurer pays only a portion of the claimed amount, and claim delay, where the insurer fails to process the claim within the time frame mandated by IRDAI regulations.

Insurance is fundamentally a contract of utmost good faith (uberrima fides) between the insurer and the insured. Both parties are expected to act honestly and disclose all material facts. When an insurer rejects a claim, it is asserting that the contract terms have been breached or that the loss falls outside the scope of coverage. However, not every rejection is legitimate — insurers sometimes deny valid claims on flimsy or technical grounds, and this is where the law intervenes to protect policyholders.

Did You Know?

According to IRDAI's annual reports, thousands of insurance claims are rejected every year across health, life, and motor segments. A significant percentage of these rejections are overturned on appeal through the Insurance Ombudsman or Consumer Forums, indicating that many initial rejections are unjustified.

Common Reasons for Claim Rejection

Understanding why insurance claims get rejected is the first step in fighting back effectively. While each case is unique, the following are the most frequently cited grounds by insurers across health, life, motor, and property insurance policies:

Non-Disclosure or Misrepresentation

This is the most common reason for claim rejection, particularly in health and life insurance. Insurance contracts require the insured to disclose all material facts at the time of purchasing the policy. If you failed to disclose a pre-existing medical condition, a history of smoking or alcohol use, a prior claim with another insurer, or any other fact that would have influenced the insurer's decision to issue the policy or determine the premium, the insurer may invoke non-disclosure to deny the claim. However, under Section 45 of the Insurance Act, 1938, a life insurance policy cannot be repudiated on grounds of misrepresentation after three years from the date of issuance.

Policy Exclusions

Every insurance policy contains a list of exclusions — specific events, conditions, or circumstances that are not covered. For health insurance, common exclusions include cosmetic surgery, dental treatment, pre-existing diseases during the waiting period, and self-inflicted injuries. For motor insurance, driving under the influence of alcohol, using the vehicle for purposes other than declared (e.g., commercial use on a private policy), or driving without a valid licence are common exclusion grounds. Insurers frequently cite policy exclusions to deny claims, and policyholders must carefully review the exclusion clauses in their policy documents.

Lapse in Premium Payment

If you fail to pay your insurance premium by the due date and the grace period (typically 15 to 30 days, depending on the policy type) has expired, the policy lapses and the insurer is not obligated to honour any claim made during the lapsed period. This is particularly common in life insurance and health insurance. However, many policies offer a revival option that allows policyholders to reinstate a lapsed policy by paying the outstanding premium along with interest or penalties, subject to certain conditions.

Delayed Claim Filing

Insurance policies prescribe specific time limits for filing a claim after the insured event occurs. For health insurance, the policyholder or hospital is typically required to notify the insurer within 24 to 48 hours for cashless claims and within a specified period (often 15 to 30 days) for reimbursement claims. For motor insurance, the claim must usually be filed within a reasonable time after the accident. Failure to file within these timelines — without a justifiable reason — can result in the claim being denied.

Insufficient Documentation

Insurers require comprehensive documentation to process a claim. For health insurance, this includes hospitalisation records, discharge summaries, diagnostic reports, prescriptions, original bills, and the claim form. For life insurance death claims, the requirements include the death certificate, policy document, claimant's identity proof, and sometimes a post-mortem report. If you fail to submit the required documents or if the documents contain discrepancies, the insurer may reject the claim. However, IRDAI regulations mandate that the insurer must clearly communicate what documents are required and give the claimant an opportunity to submit them before making a final decision.

Important

If your claim has been rejected due to "insufficient documentation," do not assume the matter is closed. IRDAI regulations require the insurer to specify exactly which documents are missing and provide you a reasonable opportunity to furnish them. A blanket rejection on documentation grounds without specifying the deficiency may itself be a violation of IRDAI guidelines.

Your Rights as a Policyholder

Indian law provides policyholders with a strong set of rights that insurance companies are bound to respect. Under the Insurance Act, 1938, the IRDAI (Protection of Policyholders' Interests) Regulations, 2017, and the Consumer Protection Act, 2019, you have the following key rights:

- Right to a Written Explanation: The insurer must provide a clear, written reason for rejecting your claim, citing specific policy terms or clauses.

- Right to Fair Claim Settlement: IRDAI regulations mandate that insurers settle claims promptly, fairly, and transparently. Health insurance claims must be settled within 30 days of receiving all necessary documents.

- Right to Information: You have the right to receive a copy of your policy document, claim status updates, and all correspondence related to your claim.

- Right to Grievance Redressal: Every insurer is required to have an internal grievance redressal mechanism. Beyond this, you can approach the IRDAI, the Insurance Ombudsman, or the Consumer Forum.

- Right Against Unfair Rejection: A claim cannot be rejected on grounds that were not clearly excluded in the policy or on technicalities that do not materially affect the validity of the claim.

- Right to Free-Look Period: For new policies, IRDAI mandates a 15-day (30-day for online policies) free-look period during which you can cancel and get a full refund if you disagree with the terms.

These rights form the legal foundation on which you can challenge an unfair insurance claim rejection. A legal notice asserting these rights often compels the insurer to reconsider and settle the claim to avoid regulatory scrutiny and consumer court proceedings.

Legal Framework

Understanding the legal provisions that govern insurance contracts and claim settlement in India is essential for drafting an effective legal notice. The three primary legislations are:

Insurance Act, 1938

The Insurance Act, 1938 is the foundational legislation governing the insurance industry in India. Section 45 is particularly important for policyholders — it restricts the insurer's ability to repudiate a life insurance policy. After the policy has been in force for three years, the insurer cannot challenge the policy on grounds of misstatement or non-disclosure unless it can prove that the statement was material, false, and made with the knowledge of the policyholder, and that the insurer was aware of the fraud. Section 38 deals with assignment and transfer of policies, while Section 39 governs nominations. Together, these provisions create a framework that prevents insurers from using technical loopholes to deny legitimate claims.

IRDAI (Protection of Policyholders' Interests) Regulations, 2017

The IRDAI (Protection of Policyholders' Interests) Regulations, 2017 lay down detailed guidelines that every insurer must follow regarding policy servicing, claim processing, and grievance redressal. Key provisions include: the insurer must settle or reject a claim within 30 days of receiving all required documents; if further investigation is needed, it must be completed within 90 days; the insurer must pay interest on delayed claim settlements at a rate of 2% above the bank rate; the insurer must appoint a Grievance Redressal Officer and resolve complaints within 15 days; and all rejections must be accompanied by specific, written reasons.

Consumer Protection Act, 2019

Insurance services fall squarely within the definition of "service" under the Consumer Protection Act, 2019. This means any deficiency in insurance service — including wrongful claim rejection, delay in settlement, or unfair policy terms — can be challenged before the Consumer Disputes Redressal Commissions (District, State, or National, depending on the claim value). Policyholders can seek compensation for financial loss, mental agony, harassment, and litigation costs. The Act also provides for mediation as an alternative dispute resolution mechanism.

The insurance company cannot repudiate the claim on hyper-technical grounds. The terms of the insurance policy have to be read as a whole and the insurer is expected to act with utmost good faith while settling the claims of the policyholders.

— National Consumer Disputes Redressal Commission (NCDRC), various rulings

When to Send a Legal Notice to an Insurance Company

A legal notice is a formal communication that puts the insurance company on notice of your intention to pursue legal remedies if the dispute is not resolved. You should consider sending a legal notice in the following situations:

- Your insurance claim has been rejected and you believe the rejection is unjustified or based on incorrect facts.

- The insurer has short-settled your claim — paying significantly less than the amount you are entitled to under the policy.

- The insurer has delayed the claim settlement beyond the time limits prescribed by IRDAI regulations (30 days for standard claims, 90 days for investigated claims).

- The insurer has failed to provide a clear written reason for the rejection, violating IRDAI guidelines.

- The rejection is based on an exclusion clause that was not clearly communicated to you at the time of purchasing the policy.

- Your internal grievance complaint to the insurer has gone unresolved or unanswered within the prescribed 15-day period.

- The insurer has demanded unreasonable or irrelevant documents to stall the claim process.

Pro Tip

Before sending a legal notice, exhaust the insurer's internal grievance mechanism first. This is not a legal requirement, but having proof that you attempted resolution through proper channels significantly strengthens your position in any subsequent legal proceedings. Keep a record of all grievance reference numbers and correspondence.

Insurance Claim Wrongfully Rejected?

OpenVakil's AI-powered platform helps you draft a professional legal notice to your insurance company in minutes. Answer a few simple questions and get a lawyer-reviewed notice ready to send.

Draft Your Legal Notice NowKey Elements of an Insurance Legal Notice

A well-drafted legal notice to an insurance company must be precise, legally sound, and backed by documentary evidence. Here are the essential elements your notice should include:

- Sender's Details: Full name, address, policy number, and contact information of the policyholder (or nominee/claimant).

- Recipient's Details: Name and designation of the insurer's grievance officer, the registered office address of the insurance company, and the branch office details (if applicable).

- Policy Details: Policy number, type of insurance (health, life, motor, property), date of policy inception, premium amount, and sum insured.

- Claim Details: Claim number, date of the insured event (hospitalisation, death, accident, property damage), date the claim was filed, and the amount claimed.

- Chronological Statement of Facts: A clear, factual narrative of events — from the insured event to the claim filing, any correspondence with the insurer, and the rejection or delay.

- Grounds of Challenge: Specific reasons why the rejection is unjustified, referencing the policy terms, IRDAI regulations, the Insurance Act, and relevant judicial precedents.

- Supporting Documents: List of documents enclosed or relied upon — policy document, claim form, hospital records, FIR (for motor claims), death certificate (for life claims), previous correspondence, and the insurer's rejection letter.

- Relief Demanded: Clearly state the specific relief you are seeking — full claim settlement, interest on delayed payment, compensation for mental agony and harassment, and/or costs.

- Time Frame: A deadline of 15 to 30 days for the insurer to respond or settle the claim.

- Consequence of Non-Compliance: A clear warning that failure to settle within the given time will result in filing a complaint with the Insurance Ombudsman or Consumer Forum, and the insurer will be liable for additional costs, interest, and compensation.

Keep It Professional

Your legal notice must be firm, factual, and professional. Avoid emotional language, threats, or exaggerations. Courts and regulatory bodies take well-reasoned notices seriously and are more likely to rule in your favour when the notice demonstrates a clear understanding of the facts and the law.

Step-by-Step Process

Follow these steps to effectively challenge an insurance claim rejection in India:

- Obtain the Rejection Letter: Request a formal written rejection letter from the insurer if you have not received one. This letter must specify the exact grounds for denial as required by IRDAI regulations.

- Review Your Policy Document: Carefully read your policy terms, conditions, exclusions, and the claims procedure. Identify whether the insurer's grounds for rejection are actually supported by the policy terms.

- Gather All Evidence: Collect every relevant document — the policy document, premium receipts, claim form, medical records, hospital bills, FIR copies (for motor or theft claims), death certificate (for life insurance), photographs, and all correspondence with the insurer.

- File an Internal Grievance: Submit a formal grievance with the insurance company's Grievance Redressal Officer. Document the grievance reference number and follow up if there is no response within 15 days.

- Draft the Legal Notice: Prepare a comprehensive legal notice covering all the key elements described above. You may draft this yourself, engage an advocate, or use OpenVakil's AI-powered platform for fast, lawyer-reviewed drafting.

- Send via Registered Post / Speed Post: Dispatch the notice through registered post or speed post with acknowledgment due (AD) to the insurer's registered office. Retain the postal receipt and tracking details as proof of delivery.

- Send a Copy via Email: Additionally, email a scanned copy to the insurer's official grievance email address and the designated grievance officer. Request a read receipt.

- Wait for Response: Allow the stipulated 15 to 30 days for the insurer to respond. Many claims are reconsidered and settled at this stage.

- Escalate if Necessary: If the insurer does not respond or reiterates the rejection, escalate the matter to the IRDAI IGMS portal, the Insurance Ombudsman, or the appropriate Consumer Forum.

Need Help Drafting Your Insurance Legal Notice?

Don't navigate the legal complexities alone. OpenVakil generates a professionally worded, legally accurate notice tailored to your specific insurance dispute — health, life, motor, or property.

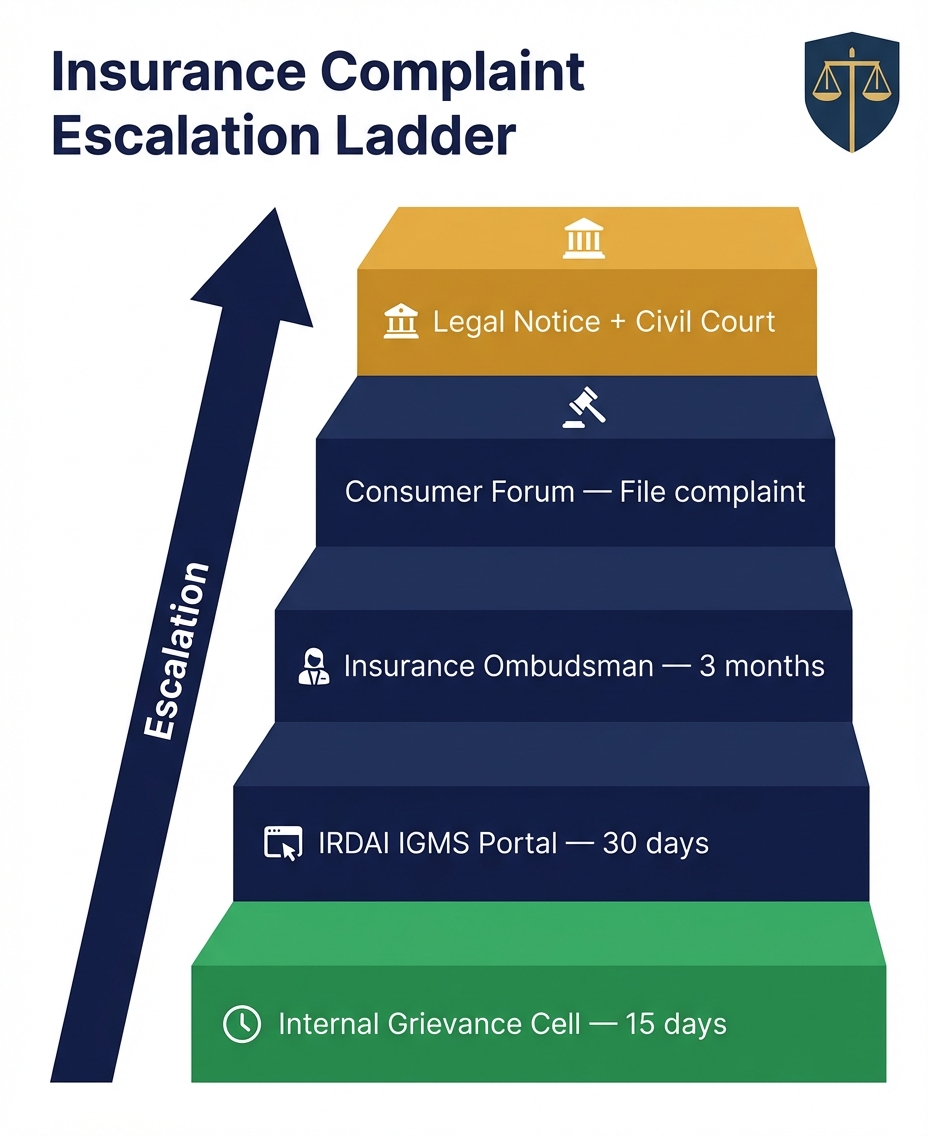

Start Drafting NowGrievance Redressal Mechanisms

India has a multi-layered grievance redressal system specifically designed for insurance disputes. Understanding each level helps you choose the most effective course of action based on the nature and value of your claim.

Internal Grievance Cell of the Insurance Company

Every insurance company in India is required by IRDAI to establish an internal grievance redressal mechanism. This is typically the first step. You must submit a written complaint to the insurer's Grievance Redressal Officer (GRO), whose details are available on the insurer's website and policy documents. The insurer is mandated to acknowledge the complaint within 3 working days and resolve it within 15 days. If you are not satisfied with the resolution, you can escalate to higher authorities within the company before approaching external forums.

IRDAI Integrated Grievance Management System (IGMS)

The IRDAI Integrated Grievance Management System (IGMS) is an online platform where policyholders can register complaints against insurance companies. Accessible at igms.irda.gov.in, the portal allows you to file a complaint, upload supporting documents, and track the status of your grievance. Once a complaint is filed, IRDAI forwards it to the concerned insurer for resolution. While IRDAI does not directly adjudicate disputes, its intervention carries significant regulatory weight, and insurers often settle claims promptly to avoid regulatory action. You can also call the IRDAI toll-free number 155255 or send a complaint via email.

Insurance Ombudsman

The Insurance Ombudsman is a quasi-judicial authority established under the Insurance Ombudsman Rules, 2017 to resolve insurance complaints in a cost-effective, expeditious, and impartial manner. There are 17 Insurance Ombudsman offices across India, each covering specific states and union territories. You can approach the Ombudsman if your complaint pertains to claim rejection, delay in claim settlement, disputes regarding premium, or any other policyholder grievance — provided the claim value does not exceed Rs. 50 lakh (including expenses and compensation). The Ombudsman process is free of cost, does not require a lawyer, and the decision is binding on the insurer (though the policyholder can reject it and approach the Consumer Forum). Complaints must be filed within one year of the insurer's final rejection.

Ombudsman Advantage

The Insurance Ombudsman is often the fastest and most cost-effective route for resolving insurance disputes. The process is free, decisions are typically delivered within 3 months, and the insurer is legally bound by the Ombudsman's award. However, you must have first approached the insurance company's grievance cell and either received an unsatisfactory response or no response within 30 days.

Consumer Forum

If the Insurance Ombudsman's decision is not satisfactory or if the claim value exceeds Rs. 50 lakh, you can file a complaint before the appropriate Consumer Disputes Redressal Commission under the Consumer Protection Act, 2019. The District Commission handles claims up to Rs. 1 crore, the State Commission handles claims between Rs. 1 crore and Rs. 10 crore, and the National Commission (NCDRC) handles claims exceeding Rs. 10 crore. Consumer Forums can order the insurer to pay the claim amount, interest on delayed settlement, compensation for mental agony and harassment, litigation costs, and even punitive damages in cases of gross unfair trade practices. Complaints must be filed within two years of the cause of action.

Common Mistakes to Avoid

When challenging an insurance claim rejection, policyholders often make mistakes that weaken their case. Avoiding these common pitfalls can significantly improve your chances of a successful outcome:

- Accepting the Rejection Without Question: Many policyholders assume the insurer's decision is final. It is not. You have multiple legal avenues to challenge an unfair rejection.

- Not Reading the Rejection Letter Carefully: The rejection letter contains the specific grounds for denial. Understanding these grounds is essential to formulating your response and identifying any errors or misinterpretations by the insurer.

- Delaying Action: Time limits apply at every stage — 15 days for internal grievance response, 1 year for the Insurance Ombudsman, and 2 years for the Consumer Forum. Delaying action can result in losing your right to challenge the rejection.

- Not Maintaining Documentation: Failing to keep copies of the policy document, premium receipts, claim forms, medical records, correspondence, and the rejection letter makes it extremely difficult to build a strong case.

- Sending an Informal Complaint Instead of a Legal Notice: A casual email or phone call does not carry the same legal weight as a formal legal notice sent via registered post. A legal notice signals your seriousness and puts the insurer on formal legal notice.

- Not Citing Relevant Laws and Regulations: A legal notice that merely states your dissatisfaction without referencing the specific provisions of the Insurance Act, IRDAI regulations, or Consumer Protection Act is far less effective.

- Approaching the Wrong Forum: Filing directly with the Consumer Forum without first exhausting the insurer's internal grievance mechanism or the Insurance Ombudsman can lead to delays and procedural complications.

- Exaggerating or Misrepresenting Facts: Always be truthful and accurate in your legal notice and complaints. Any misrepresentation can be used against you and undermine your credibility.

Key Takeaway

The most successful insurance claim challenges are built on three pillars: thorough documentation, timely action, and accurate citation of legal provisions. If you have these three elements, you are in a strong position to get your claim settled.

How OpenVakil Helps

Fighting an insurance claim rejection can feel overwhelming, especially when you are dealing with the financial and emotional stress that often accompanies such situations. OpenVakil simplifies the entire process by combining cutting-edge AI technology with legal expertise to help you take effective action.

With OpenVakil, you can generate a professional, legally sound legal notice tailored to your specific insurance dispute in minutes. Whether your claim has been rejected by a health insurer, a life insurance company, a motor insurer, or a property insurer — our platform guides you through a series of simple questions about your policy, the claim, the rejection, and the relief you seek. The AI engine then drafts a comprehensive notice citing the relevant provisions of the Insurance Act, IRDAI regulations, and the Consumer Protection Act.

- AI-Powered Drafting: Get a professionally worded insurance legal notice generated in minutes, tailored to the specific facts and legal issues in your case.

- Lawyer-Reviewed Quality: Every notice is reviewed for legal accuracy, ensuring it cites the correct statutory provisions and meets professional standards.

- Coverage Across All Insurance Types: Whether it is health, life, motor, property, or travel insurance — OpenVakil handles claim rejection notices for all categories.

- Affordable & Transparent Pricing: Access high-quality legal notice drafting at a fraction of the cost of traditional legal services, with no hidden charges.

- End-to-End Guidance: From drafting the notice to advice on sending it, filing with the Insurance Ombudsman, and approaching the Consumer Forum, OpenVakil supports you through every step.

Don't Let Your Insurance Company Get Away With It

You paid your premiums on time. You deserve your claim. Draft a powerful legal notice with OpenVakil and take the first step toward getting the settlement you are entitled to.

Get Started for FreeAn insurance policy is a promise — a promise to stand by you in your time of need. When an insurer breaks that promise by wrongfully rejecting your claim, the law is on your side. Armed with the right knowledge, proper documentation, and a well-drafted legal notice, you can hold any insurance company accountable. Remember, a legal notice is often all it takes to compel an insurer to reconsider and settle your claim. Take action today and protect your rights as a policyholder.