A bounced cheque is more than just an inconvenience — it is a criminal offence under Indian law. If someone has issued you a cheque that has been returned unpaid by the bank, you have the legal right to initiate criminal proceedings against the drawer under Section 138 of the Negotiable Instruments Act, 1881. However, before you can file a complaint in court, the law mandates that you first send a cheque bounce legal notice demanding payment. This guide walks you through everything you need to know about the cheque bounce notice process, the strict time limits involved, and how to protect your legal rights.

What Is a Cheque Bounce?

A cheque bounce (also called cheque dishonour) occurs when a bank refuses to honour a cheque presented for payment. The most common reason is insufficient funds in the drawer's account, but cheques can also bounce due to a mismatch of signature, overwriting, a stale date, or a stop-payment instruction from the drawer.

When a cheque bounces, the bank issues a cheque return memo to the payee's bank, stating the reason for dishonour. This memo is a crucial document — it serves as primary evidence if you decide to pursue legal action under Section 138 of the Negotiable Instruments Act.

What Is a Cheque Return Memo?

A cheque return memo is a slip issued by the bank when a cheque is dishonoured. It states the reason for the bounce (e.g., "Insufficient Funds", "Exceeds Arrangement", "Account Closed"). Always preserve this document carefully — it is the foundation of your Section 138 case.

Understanding Section 138 of the Negotiable Instruments Act

Section 138 of the Negotiable Instruments Act, 1881 makes the dishonour of a cheque a criminal offence. The provision was introduced by an amendment in 1988 to strengthen the credibility of cheques as a reliable mode of payment in commercial transactions. The law ensures that when someone issues a cheque to discharge a legally enforceable debt or liability, and that cheque is returned unpaid, the drawer can be held criminally liable.

The Supreme Court of India has consistently upheld the importance of Section 138, observing that it serves a vital public purpose — maintaining faith in the efficacy of banking operations and negotiable instruments. In Dashrath Rupsingh Rathod v. State of Maharashtra (2014) and subsequent legislative amendments, the framework for cheque bounce cases has been refined to balance the interests of both payees and drawers.

When Does Section 138 Apply?

For a cheque bounce to be prosecutable under Section 138, all of the following conditions must be satisfied:

- The cheque must have been issued to discharge a legally enforceable debt or liability. Cheques given as gifts, security, or for purposes not linked to an existing debt do not attract Section 138.

- The cheque must have been presented to the bank within its validity period. A cheque is valid for 3 months from the date written on it (as per RBI guidelines effective from April 2012; previously it was 6 months).

- The cheque must have been returned unpaid (dishonoured) by the bank. The dishonour must be due to insufficient funds or because the amount exceeds the arrangement made with the bank.

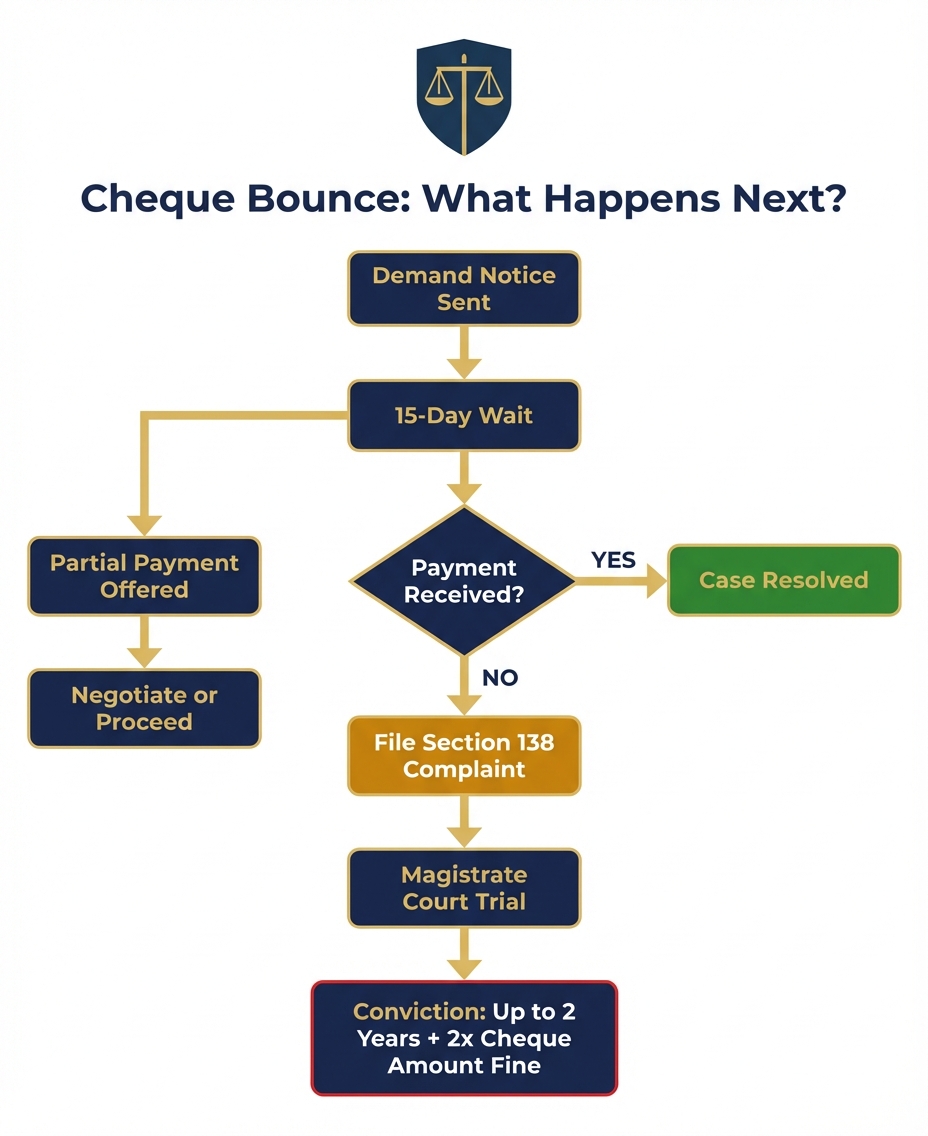

- The payee must send a written demand notice to the drawer within 30 days of receiving the cheque return memo. This notice must demand payment of the cheque amount.

- The drawer must fail to make the payment within 15 days of receiving the demand notice. Only after this 15-day period expires without payment can the payee file a complaint.

Important: Reason for Dishonour Matters

Section 138 applies only when a cheque bounces due to "insufficient funds" or the amount "exceeding the arrangement" with the bank. If the cheque bounces for other reasons — such as signature mismatch, account closed, or stop payment — the criminal offence under Section 138 may not be directly attracted. However, in practice, courts have taken a broad view, and you should consult a lawyer for specific circumstances.

Critical Time Limits You Must Follow

The cheque bounce process under Section 138 is governed by strict time limits. Missing even one deadline can render your entire case invalid. Here is the complete timeline you must adhere to:

The 30-Day Demand Notice

Within 30 days of receiving information from the bank that the cheque has been dishonoured (i.e., from the date you receive the cheque return memo), you must send a written demand notice to the drawer. This notice must demand that the drawer pay the cheque amount. The 30-day period is calculated from the date you receive the return memo, not the date the cheque was presented.

The 15-Day Waiting Period

After sending the demand notice, you must wait for 15 days to allow the drawer an opportunity to make the payment. This 15-day period is counted from the date the drawer receives the notice. If the drawer makes full payment within these 15 days, you cannot file a criminal complaint. If the drawer refuses to accept the notice or it is returned with the endorsement "refused" or "not claimed", the notice is still considered to have been served.

Pro Tip: Use Registered Post with AD

Always send the cheque bounce notice via Registered Post with Acknowledgement Due (RPAD). The postal receipt and the acknowledgement card serve as proof that the notice was dispatched and delivered. Courts treat RPAD as valid service of notice even if the addressee refuses to accept it.

The 30-Day Complaint Filing Window

If the drawer does not make the payment within 15 days of receiving the notice, you must file a criminal complaint in the appropriate Magistrate's court within 30 days from the expiry of the 15-day notice period. This complaint window is strict — if you miss it, you lose the right to prosecute under Section 138 for that particular cheque dishonour.

The entire timeline from cheque bounce to filing a complaint is roughly 75 days: 30 days to send notice + 15 days waiting period + 30 days to file complaint. Every day counts.

— Summary of Section 138 Timeline

Step-by-Step Process for Sending a Cheque Bounce Notice

Follow these steps carefully to ensure your cheque bounce notice is legally valid and your right to file a criminal complaint is preserved:

- Collect and preserve all documents: Gather the original bounced cheque, the cheque return memo from the bank, your bank statement showing the cheque deposit and return, and any underlying agreement, invoice, or communication that establishes the debt or liability.

- Draft the demand notice: Prepare a formal legal notice addressed to the drawer. The notice must clearly state the facts — the cheque details, the reason for dishonour, the underlying debt, and a demand for payment of the full cheque amount within 15 days of receipt.

- Get the notice reviewed by a lawyer: While not legally mandatory, having the notice drafted or reviewed by an advocate adds weight and ensures legal accuracy. Many payees send notices through their advocate, which is common practice.

- Send the notice via Registered Post with Acknowledgement Due (RPAD): Dispatch the notice to the drawer's address as mentioned on the cheque or any known address. Keep the postal receipt safely — it is proof of dispatch.

- Wait for the 15-day period to expire: Count 15 days from the date the notice is delivered (or deemed to be delivered). During this period, the drawer may make the payment.

- If unpaid, file a criminal complaint: If the drawer fails to pay within 15 days, file a complaint under Section 138 in the competent Magistrate's court within 30 days from the expiry of the notice period.

Draft Your Cheque Bounce Notice in Minutes

OpenVakil's AI-powered platform helps you create a legally sound cheque bounce notice under Section 138. Answer a few simple questions, and get a lawyer-reviewed notice ready to send.

Create Your Notice NowEssential Elements of a Cheque Bounce Notice

A legally effective cheque bounce notice must contain the following essential elements. Omitting any of these can weaken your case or give the drawer grounds to challenge the notice:

- Full name and address of the payee (sender) and the drawer (recipient) as they appear in relevant records.

- Details of the cheque: cheque number, date, amount (in figures and words), name of the issuing bank, and branch.

- Date of presentation of the cheque to the bank and the date of dishonour as per the cheque return memo.

- Reason for dishonour as stated in the cheque return memo (e.g., "Insufficient Funds").

- Description of the underlying debt or liability for which the cheque was issued — referencing any agreement, invoice, loan, or transaction.

- A clear demand for payment of the full cheque amount within 15 days of receipt of the notice.

- A statement of legal consequence: a warning that failure to pay will result in criminal proceedings under Section 138 of the Negotiable Instruments Act.

- Date and place of issuing the notice, along with the signature of the payee or their advocate.

Do Not Demand More Than the Cheque Amount

The demand notice must ask for payment of the cheque amount only. Demanding interest, damages, or any amount exceeding the face value of the cheque in the Section 138 notice can create complications. You can claim interest and compensation separately when filing the complaint in court.

What Happens After Sending the Notice?

Once you have dispatched the cheque bounce legal notice, there are three possible outcomes. Your next steps depend on how the drawer responds:

Scenario 1: Payment Is Received

If the drawer makes the full payment within 15 days of receiving the notice, the matter is resolved. You cannot file a criminal complaint under Section 138 once the payment is made within the stipulated period. Issue a receipt acknowledging the payment and consider the matter closed. This is the best outcome for both parties, as it avoids the time and expense of litigation.

Scenario 2: No Response from the Drawer

If the drawer ignores the notice and makes no payment within 15 days, this constitutes a cause of action under Section 138. You can now file a criminal complaint before the competent Magistrate within 30 days from the expiry of the 15-day notice period. The court will take cognizance of the offence and issue summons to the drawer.

Scenario 3: Partial Payment Offered

If the drawer offers only a partial payment, you are not obligated to accept it. Under Section 138, the legal obligation is to pay the full cheque amount within 15 days. A partial payment does not extinguish the offence. You may accept the partial payment without prejudice to your rights and still file a complaint for the remaining amount, or you may refuse the partial payment and proceed with the full complaint. Consult a lawyer for the best strategy in your specific situation.

Keep Records of All Communication

Maintain copies of the notice, postal receipts, acknowledgement cards, any replies from the drawer, and records of partial payments. These documents form critical evidence when filing and arguing the case in court.

Filing a Criminal Complaint Under Section 138

If the drawer fails to pay within 15 days of receiving your demand notice, you can initiate criminal proceedings. Here is what the complaint process involves:

- Jurisdiction: The complaint must be filed in the court that has territorial jurisdiction over the place where the cheque was delivered for collection (i.e., where your bank branch is located), as clarified by the 2015 amendment to the NI Act.

- Filing the complaint: Prepare a written complaint supported by an affidavit. Attach copies of the bounced cheque, cheque return memo, the demand notice, postal receipt, acknowledgement card (if available), and any evidence of the underlying debt.

- Court process: The Magistrate examines the complaint and, if satisfied, issues summons to the accused (drawer). The accused must appear before the court. If the accused pleads not guilty, a trial follows.

- Examination of the complainant: Under Section 145 of the NI Act, the complainant's evidence can be given by way of affidavit, which speeds up proceedings. The accused has the right to cross-examine the complainant.

- Defence and verdict: The accused may present a defence — for example, that the cheque was not issued for a debt, or that the notice was not properly served. If the court finds the accused guilty, it passes the sentence.

Section 138 cases are tried as summary trials under Section 143 of the NI Act, which means the trial should be concluded as expeditiously as possible. Courts have been directed to try to complete these cases within six months, though delays are common in practice.

Penalties and Punishment for Cheque Bounce

The penalties for a cheque bounce offence under Section 138 are significant and serve as a strong deterrent:

- Imprisonment: The convicted drawer may face imprisonment for a term that may extend up to 2 years.

- Fine: The court may impose a fine that may extend up to twice the amount of the cheque.

- Both: The court may impose both imprisonment and fine.

- Compensation: Under Section 357 of the Code of Criminal Procedure (now Section 395 of the Bharatiya Nagarik Suraksha Sanhita, 2023), the court can direct the accused to pay compensation to the complainant.

Interim Compensation Under Section 143A

Under Section 143A of the NI Act (inserted by the 2018 amendment), the court may order the drawer to pay interim compensation of up to 20% of the cheque amount during the pendency of the case. This provides relief to the complainant even before the final verdict. If the accused is acquitted, the interim compensation must be refunded with interest.

It is important to note that Section 138 is a compoundable offence, meaning the parties can settle the matter at any stage of the proceedings with the permission of the court. Many cheque bounce cases are resolved through negotiation and settlement before a final verdict is passed.

Common Mistakes to Avoid

Filing a cheque bounce case requires strict adherence to procedure. Here are the most common mistakes that payees make — any of these can result in the dismissal of your case:

- Sending the notice after 30 days: The demand notice must be sent within 30 days of receiving the cheque return memo. Even a single day's delay can be fatal to your case.

- Not sending the notice via RPAD: Sending the notice by ordinary post, courier, or email alone may create problems proving service. Always use Registered Post with Acknowledgement Due as the primary mode.

- Vague or incomplete notice: The notice must clearly state the cheque details, amount, reason for dishonour, the underlying debt, and a clear demand for payment. Vague notices can be challenged by the drawer.

- Demanding more than the cheque amount: Including demands for interest, damages, or mental agony in the demand notice can be used by the defence to argue that the notice is defective.

- Missing the complaint filing deadline: The complaint must be filed within 30 days after the 15-day notice period expires. Missing this window means you cannot prosecute under Section 138 for that dishonour.

- Not preserving the original cheque: The original bounced cheque is primary evidence. Losing it significantly weakens your case. Keep the original in a safe place and use photocopies for your records.

- Filing in the wrong court: The complaint must be filed in the court having jurisdiction over the place where the cheque was delivered for collection. Filing in the wrong court leads to dismissal and loss of valuable time.

- Not presenting the cheque within the validity period: If you present the cheque after the 3-month validity period has expired, it becomes a stale cheque and cannot form the basis of a Section 138 case.

Re-Presentation of the Cheque

You have the right to present the cheque again within its validity period after it bounces the first time. Each dishonour gives rise to a fresh cause of action, and a fresh 30-day notice period begins from the date of the new cheque return memo. However, this is advisable only if you believe the drawer may now have funds. Consult a lawyer before deciding on re-presentation.

How OpenVakil Simplifies the Process

Dealing with a cheque bounce can be stressful and confusing, especially when strict legal deadlines are involved. OpenVakil is designed to make the entire process simple, fast, and accessible — even if you have no legal background.

- AI-Powered Drafting: Answer a few straightforward questions about your cheque bounce situation, and OpenVakil's AI generates a comprehensive, legally accurate demand notice tailored to your specific case.

- Legally Compliant Notices: Every notice is structured to comply with the requirements of Section 138 of the NI Act, including all essential elements that courts look for.

- Lawyer Review Available: Get your notice reviewed by experienced legal professionals for added confidence and accuracy.

- Fast Turnaround: Generate your cheque bounce notice in minutes, not days. Time is critical in Section 138 cases, and OpenVakil helps you act quickly.

- Guidance at Every Step: From understanding your rights to sending the notice and knowing what to do next, OpenVakil guides you through the entire cheque bounce process.

Thousands of individuals and businesses across India have used OpenVakil to protect their rights in cheque bounce matters. Do not let tight deadlines and legal complexities prevent you from taking action.

Take Action on Your Cheque Bounce Case Today

Do not let the 30-day deadline pass. Use OpenVakil to draft and send a legally compliant cheque bounce notice under Section 138 in minutes. Protect your right to recover your money.

Start Your Cheque Bounce NoticeCheque bounce cases under Section 138 are among the most common commercial disputes in Indian courts. By understanding the law, following the correct procedure, and acting within the prescribed time limits, you can significantly improve your chances of recovering the amount owed to you. Whether you choose to handle the matter yourself or engage a lawyer, the first and most critical step is sending a proper demand notice — and that is where OpenVakil can help.